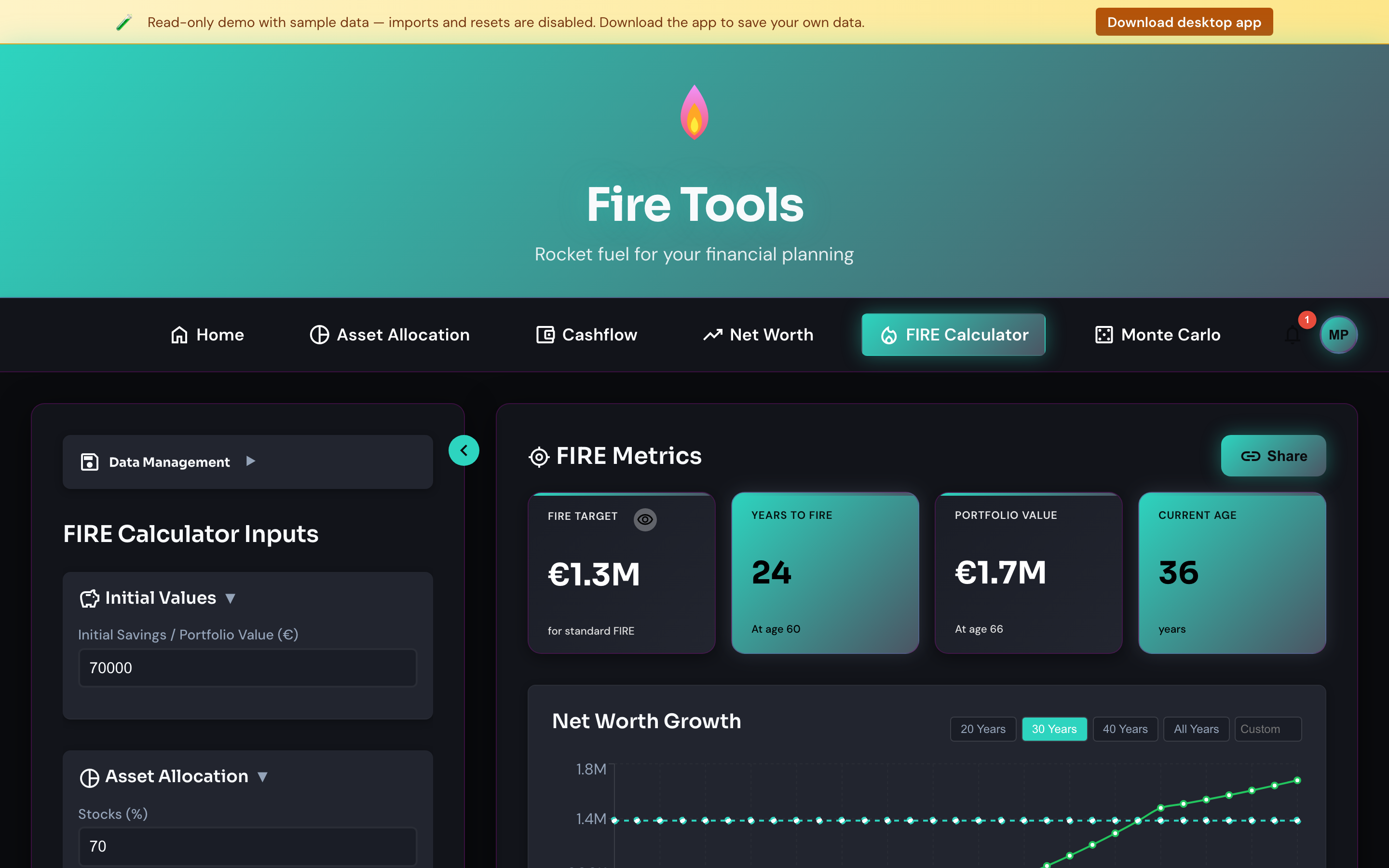

FIRE calculator

Projects how many years it takes to reach financial independence at your current savings rate, with adjustable expected return and inflation.

How to use it

- Current net worth — total of all investable assets today.

- Monthly savings — the slice of your income that goes into investments each month. Be honest with yourself.

- Annual expenses — what your life costs per year. The FIRE number is derived from this (25× by default, configurable as the withdrawal rate).

- Expected return — long-term real return on your portfolio. The default sits around 7% for a global equity-heavy mix.

- Inflation — used to keep targets in today's money.

- Withdrawal rate — the slice you pull from the portfolio each year in retirement. 4% is the classic Trinity number; lower it for a safer plan.

Every change recalculates immediately and updates the projection chart.

FIRE variants

The calculator supports five FIRE flavours. Pick one from the FIRE Type selector to change how the target number and post-FIRE behaviour are computed.

- Standard FIRE — the classic:

target = annual_expenses × years_of_expenses. After FIRE, optionally stop working (stopWorkingAtFIRE) and let the portfolio fund expenses. - Lean FIRE — minimalist lifestyle. The target is scaled down by

leanExpenseMultiplier(default0.7). Lower target ⇒ reach FIRE sooner. Formula:target = annual_expenses × leanExpenseMultiplier × years_of_expenses. - Fat FIRE — more comfortable lifestyle. The target is scaled up by

fatExpenseMultiplier(default2.0). Higher target ⇒ takes longer. Formula:target = annual_expenses × fatExpenseMultiplier × years_of_expenses. - Barista FIRE — partial retirement where a part-time job covers part of

expenses. Only the gap needs to be funded by the portfolio.

Formula:

target = max(0, annual_expenses − baristaAnnualIncome) × years_of_expenses. After FIRE, labor income is capped atbaristaAnnualIncomeand no longer grows. - Coast FIRE — save aggressively early, then stop contributing and let

compounding do the rest until a chosen retirement age.

Formula:

target = standard_target / (1 + expected_return)^(coastTargetAge − currentAge). After Coast FIRE is reached the model keeps labor income but stops new contributions; only investment yield grows the portfolio.

Notes:

- Post-FIRE expenses always use

fireAnnualExpenses— the lean/fat multipliers only affect the target, not what you actually spend in retirement. - All variants honour the existing inputs (returns, withdrawal rate, pensions, other income). Switching variants never invalidates saved data — missing fields fall back to defaults.

Reading the chart

- The line shows projected net worth year by year.

- The horizontal line is your FIRE target (

expenses / withdrawal_rate). - Where the curve crosses the target is your FIRE date.

Sharing a scenario

Inputs are encoded in the URL. Copy the URL out of the address bar and share — recipients open the same scenario without any data leaving either device.

Exporting

Use Export CSV to download the inputs and the year-by-year projection. Use Import CSV to load a previously exported file.

Caveats

- The projection is deterministic. Run the Monte Carlo simulation if you want to see how volatility affects success rate.

- The expected return is a real return (after inflation). If you input a nominal return, set inflation to zero so you don't double-count it.

Reverse FIRE Calculator

The companion Reverse FIRE page (linked from the FIRE Calculator header,

or navigate to /reverse-fire-calculator) flips the question around: instead

of asking when you'll reach FIRE, you pick a target retirement age and

the tool tells you how much you must save each month to get there.

Inputs:

- Target retirement age

- Current savings

- Annual FIRE expenses + withdrawal rate (defines the FIRE target)

- Expected stock, bond and cash returns (weighted by your asset allocation)

- Inflation proxy (absolute value of the cash return)

- "Inflate FIRE target to retirement year" toggle — when on, the target is expressed in future euros; when off, both target and returns are treated as real values.

Output:

- Required monthly and annual savings (annuity-due — contributions assumed at the start of each year)

- Projected future value of your current savings alone

- The FIRE target you're aiming at

- An "already on track" badge when no further contributions are needed

The page shares its inputs with the forward FIRE calculator via the same encrypted cookie storage, so toggling between the two views never loses your numbers.